KUALA LUMPUR OFFICE MARKET REVIEW

by Rahim & Co Research Sdn Bhd

The main driver of growth for

the office space market in Kuala Lumpur has typically been the nation's high

economic growth. Demand for office space was at constant high during the early

90's but changed significantly due to the regional economic crisis in 1998. The

demand for office space declined, made worse by the oversupply situation and

poor absorption rate of office space. This has been the scenario of the KL

office market since 1998 until recently, where economic growth has picked up and

gradually renewing interest in the office property market.

The domestic economy expanded by 7.1% in 2004, charting the most impressive economic growth since year 2000. Last year's GDP growth was the highest when compared to the previous two years GDP figure of 4.1% (year 2002) and 5.3% (year 2003). The private sector continued to be forerunner of the economic growth, providing the platform and impetus for sustained expansion. Sectors that have contributed to the economic expansion were manufacturing, services and higher prices for primary commodities.

The strong expansion in the

manufacturing sector is attributed to the higher demand from export and

domestic-oriented industries. Stable employment market and higher consumer

spending, coupled with higher tourism activities drove the growth in the

services sector. The expansion in finance, insurance,

real estate and business services sub-sector, telecommunications industry,

private education and private healthcare services further boost the growth of

the services sector.

In addition to strong GDP

growth, other economic indicators also showed positive signs with unemployment

rate remained unchanged from the last 2 years figure of 3.5% and higher demand

for employment with the expansion of private investment. Consumer Price Index

(CPI) growth rate has remained stable in 2004 at 1.4%, one of the lowest in the

region.

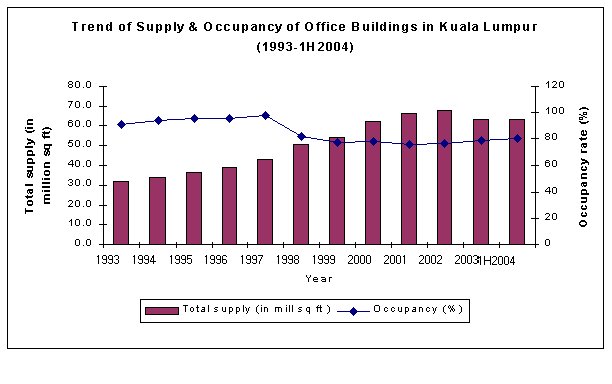

The 12-year trend of supply and occupancy for purpose-built offices in Kuala Lumpur

|

Year |

No. of building

|

Total supply (sf)

|

Occupancy |

|

|

(sf) |

% |

|||

|

1993 |

215 |

31,926,541 |

29,062,671 |

91 |

|

1994 |

223 |

33,765,645 |

31,748,709 |

94 |

|

1995 |

232 |

36,359,048 |

34,663,320 |

95.3 |

|

1996 |

144 |

38,809,720 |

36,933,415 |

95.2 |

|

1997 |

252 |

42,576,668 |

41,606,143 |

97.7 |

|

1998 |

272 |

50,250,453 |

41,251,071 |

82.1 |

|

1999 |

284 |

54,111,026 |

41,626,239 |

76.9 |

|

2000 |

355 |

62,418,595 |

48,431,111 |

77.6 |

|

2001 |

373 |

66,046,645 |

49,641,955 |

75.2 |

|

2002 |

376 |

67,573,945 |

51,326,688 |

76.0 |

|

2003 |

378 |

68,095,176

|

53,382,270 |

78.4 |

|

1H2004* |

376 |

63,270,592 |

50,804,230 |

80.3 |

Note: * Half-yearly figure as at June 2004

Source: Property Market Reports 1993-1H2004

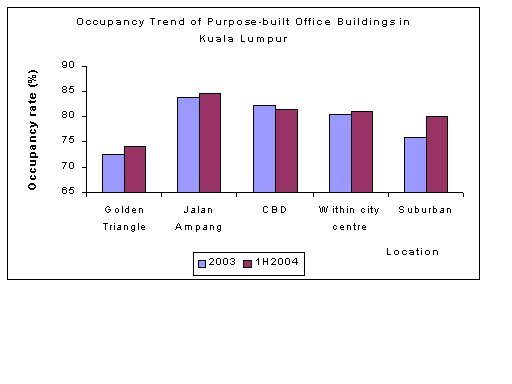

In 1H2004, there was a decline in the occupancy rates for buildings in the Central Business District (CBD) for older office buildings. Darby. Based on a y-o-y comparison, average occupancy rate in CBD declined by 0.8% from 82.3% in year 2003 to 81.5% in year 2004.

For offices located along Jalan Ampang, occupancy rose to 84.6% in year 2004, the highest occupancy rate reflecting market's preference and its popularity, particularly for offices located near KLCC Twin Towers. Offices in the suburban area of Bangsar and Damansara recorded significant rise of 4.2%, from 75.8% (year 2003) to 80% (1H2004).

Generally, the rental market remained stable with some office buildings recording mixed performance in 2004. With the improved market sentiment on the property and investment front, prime office buildings in Golden Triangle and Jalan Ampang managed to secure good rentals, ranging between RM5.00- RM8.00 psf. Older buildings such as Bangunan MAS and Wisma Haw Par in the Golden Triangle, declined about 4%-5% from 2003 to the current rate of RM3.00-3.50 psf and RM1.80 to RM2.00 psf respectively.

In the Central Business District

(CBD), rental rates were hovering at between RM1.90 - RM4.00 psf, with older

buildings such as Wisma Sime Darby and Menara Tun Razak recording lower rentals.

Office buildings in the suburban such as Wisma

Semantan remained stable with average rental at RM3.50 psf while

Menara Millenium recorded higher average

rental rate of RM4.50 psf.

|

Office Building |

Net Lettable Area

(sq ft) |

Total Value Transacted

(RM million) |

Value Transacted

(RM psf) |

|

MUI Plaza |

345,564 |

166 |

480 |

|

Menara Weld |

409,836 |

150 |

366 |

|

Wisma KFC |

175,438 |

90 |

513 |

|

Menara Cyclecarri |

397,727 |

140 |

352 |

Both yield and capital value were quite unattractive during the recession period due to lack of demand in the office market, hence, resulting in the rental pushed downward. However, the office market has since improved, in tandem with the assuring economic recovery. The current average yield for offices in Kuala Lumpur ranged from 6% to 8% depending on the office buildings, location, rental rates etc.

MARKET OUTLOOK

With the Government's effort to promote Real Estate Investment Trusts (REITs) in Malaysia, there is definitely renewed interest on the investment front for commercial properties in the recent few months. Coupled with the optimistic projected economic growth of 6% for this year, the office sector is looking bright again, with higher take-up anticipated from oil and gas companies, expansion of regional offices and relocation of some regional back office operations. For instance, global investment bank, Credit Suisse First Boston, expressed their confidence in the Malaysian market by committing 7,300 sq ft of office space in Menara IMC at Jalan Sultan Ismail. With the liberalisation efforts announced in Budget 2005 for the setting-up of foreign stockbroking on our local shore, we anticipate more foreign firms taking up space in prime offices in Kuala Lumpur this year. Some of the firms that have been approved to set up their offices here along with Credit Suisse are JP Morgan, CLSA, Macquarie and UBS.